📈Inflation, Now Streaming🍿

Nykaa's B2B puzzle, Honasa's discipline, Pilgrim's nerve

The government just stopped counting your DVD player. Last week, MoSPI dropped India’s new Consumer Price Index (CPI) and this is the loudest signal yet: India’s wallet now lives on a phone, and the bureaucrats finally noticed.

VCRs, tape recorders, CDs and cassettes- gone. In their place? Online streaming services, pen drives, external hard disks, and inflation data pulled from 12 online marketplaces. This is admitting that digital consumption isn’t optional anymore- it’s mainstream behaviour.

For D2C, this is the kind of boring policy move that quietly changes the weather. When inflation measurement captures streaming subscriptions, online pricing dynamics, and digital-first purchases, the “cost of living” narrative shifts toward the same playing fields where brands fight for attention and checkout.

Now let’s see what the ecosystem built this week while the statisticians were catching up.

🗞️Marketplace Buzz

Shadowfax hit ₹1,159 crore revenue with 65% growth in Q3 FY26, while profit jumped 5x to ₹35 crore, proving logistics infrastructure captures quick commerce boom without owning inventory. The company raised ₹1,907 crore via IPO in January after listing at a slight discount, showing public markets value last-mile execution over platform hype. Nine-month revenue reached ₹2,965 crore as Delhivery, XpressBees compete for D2C and quick commerce delivery.

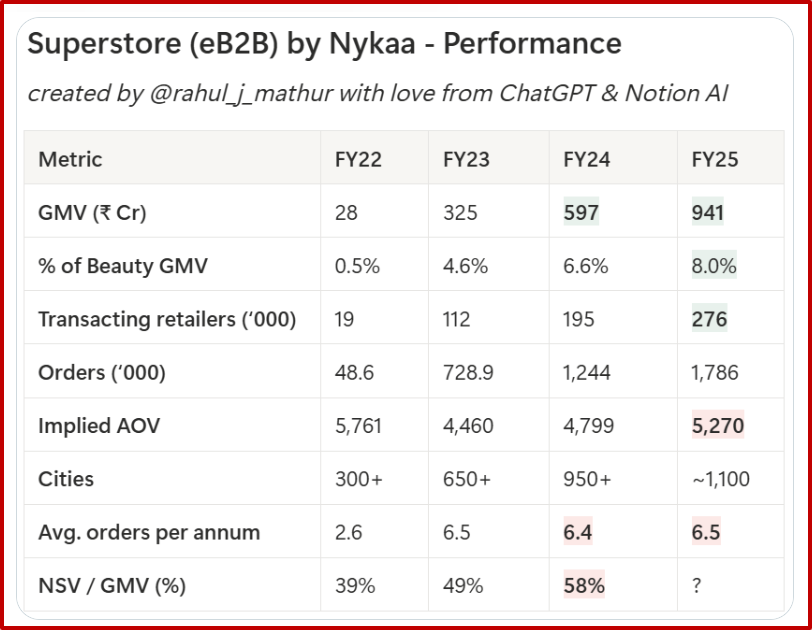

Nykaa’s SuperStore hit ₹950 Cr in GMV in FY25, serving 276,000 retailers across 1,100 cities, but those retailers place orders just 6.5 times per year, unchanged from FY24 despite adding 81,000 new accounts. The B2B2C-play weaponises brand relationships by selling ad inventory to CPG companies targeting mom-and-pop shops, turning offline retail into a captive audience. The genius is the flywheel, while the execution is retailers treating it like a backup supplier, not a primary one.

📊Infographica

🍕D2C Snippets

USV acquired 79% of Wellbeing Nutrition at ₹1,583 crore valuation with ₹170 crore FY25 revenue, showing pharma giants value nutraceutical brands despite ₹30 crore losses. HUL exited its 19.8% stake for ₹307 crore after investing ₹70 crore, earning 4x return in two years. The 2019-founded brand targets ₹450 crore revenue by FY27, proving preventive wellness attracts premium multiples.

Noise's revenue fell 24% to ₹1,048 crore in FY25 while flipping profitable, exposing the wearables trap: scale without margin discipline kills faster than controlled contraction. The Bose-backed brand slashed marketing 37% to ₹180 crore and stayed EBITDA positive at ₹18 crore, choosing survival over vanity growth. Competitor boAt hit ₹3,073 crore revenue with ₹60 crore profit, proving category winners need both.

Slurrp Farm raised ₹30 crore at ₹810 crore valuation after a two-year funding gap, exposing millet snacking’s patient capital reality: 30% revenue growth to ₹95.6 crore with ₹32.7 crore losses signals steady traction without breakout velocity. The Anushka Sharma-backed brand grew valuation 59% while keeping fundraising modest, suggesting measured confidence over momentum theatre.

GIVA hit ₹518 crore revenue with 89% growth while crossing 200 stores and achieving 50-50 online-offline split, exposing jewellery's omnichannel requirement: digital discovery needs physical conversion. Losses widened 22% to ₹72 crore as marketing hit ₹135 crore, showing scale demands sustained spend. The brand improved unit economics to ₹1.15 per rupee earned while expanding into gold and lab-grown diamonds beyond silver.

Ethera raised ₹25 crore from BlueStone after launching in 2024, exposing jewellery incumbents’ strategy to capture lab-grown diamonds through portfolio bets rather than brand pivots. The startup runs five stores across Bengaluru and Delhi while launching 200 designs monthly, targeting omnichannel expansion. BlueStone doubled its investment instead of building internally, signalling category credibility matters for new formats.

Honasa hit ₹602 crore revenue in Q3 FY26 with 16% growth while profit doubled to ₹50 crore, exposing the MamaEarth parent’s shift from hypergrowth to margin discipline after public market pressure. The company acquired men’s grooming brand Reginald for ₹195 crore while founder Varun Alagh bought ₹50 crore more equity, signalling confidence in operational momentum. Revenue grew slower than in the peak years, but profit acceleration shows portfolio consolidation is working.

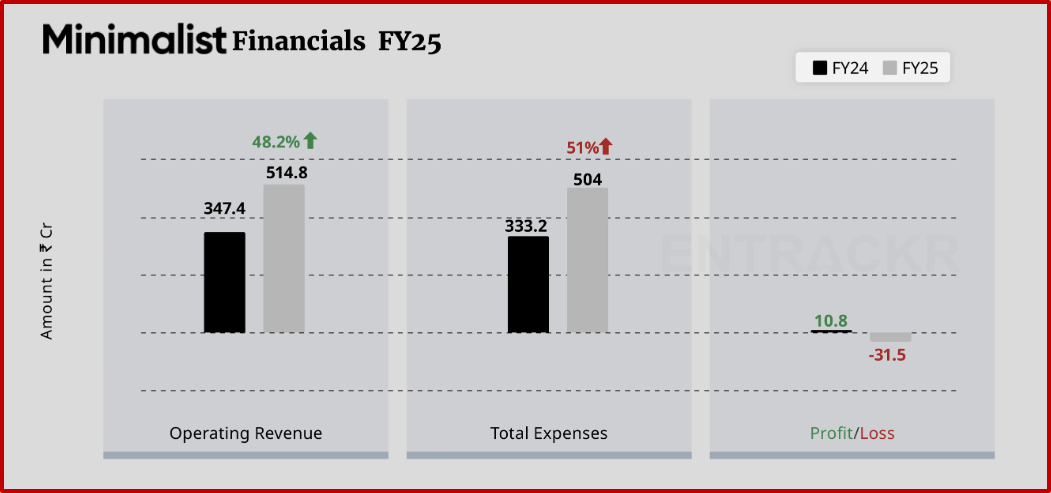

Minimalist hit ₹515 crore revenue with 48% growth in FY25 before HUL acquired 90.5% at ₹2,955 crore valuation, proving science-backed skincare scales when distribution meets ingredient credibility. The brand stayed EBITDA positive at ₹18 crore despite ₹154 crore marketing spend, showing unit economics at ₹0.98 per rupee earned.

The Man Company revenue fell 16% to ₹154 crore with ₹22 crore loss in FY25 after Emami's ₹400 crore acquisition, exposing FMCG integration friction: tripling marketing to ₹43 crore failed to prevent decline. Competitor Beardo grew to ₹214 crore with ₹13 crore profit while Ustraa declined 22% but narrowed losses, showing men's grooming category volatility. Cash dropped to ₹0.3 crore as unit economics hit ₹1.15 spent per rupee earned.

Wakefit hit ₹421 crore revenue with ₹32 crore profit in Q3 FY26 after listing loss last year, proving sleep and furniture D2C works when expenses stay disciplined at ₹397 crore. Nine-month revenue reached ₹1,145 crore with 18% growth as profit doubled sequentially from ₹16 crore.

DUSQ raised ₹24 crore for sleep regulation hardware, dismissing wearables that track sleep without fixing it as awareness theatre. The Fireside-backed startup built proprietary sleep labs testing autonomic recovery with 50 million data points, targeting biological regulation instead of score dashboards. Sleep tech stopped observing and started treating.

Renee Cosmetics raised $30 million at $200 million valuation with ₹500 crore ARR after tripling revenue in 18 months, proving that colour cosmetics scales when distribution meets product velocity. The Playbook-led round funds offline expansion into tier 1 and 2 cities while targeting ₹1,000 crore ARR in two years.

Pilgrim scaled ₹17 Cr to ₹400 Cr in three years while other beauty D2Cs bled out, and the gap isn’t formulations, it’s nerve. The brand raised $54 Mn, pushed offline when everyone preached digital, and now pulls 20% revenue from stores that other brands fear. Pilgrim’s 40% repeat rate and salon B2B prove retail discipline beats Instagram virality.

Supertails raised $30 million to perfect its Bengaluru petcare ecosystem before replicating elsewhere, stacking 30-minute delivery, 10 clinics, and at-home vet services into one full-stack model instead of chasing quick geography expansion. The former Licious executives are applying meat delivery logic to pets: own the infrastructure, then own the market.

Benny's Bowl raised $1.4 million to scale functional pet nutrition targeting allergies and weight management, exposing a repeat purchase model that looks like food but behaves like medicine. The brand doubled revenue in 12 months with 85% repeat customers, proving pet parents treat dietary fixes as recurring prescriptions without subscription friction.

Aramya raised ₹80 crore at ₹1,438 crore valuation after 13x revenue growth to ₹41 crore in FY25, proving handcrafted ethnic wear can scale like tech when distribution meets demand density. The Z47 and Accel-backed brand jumped from ₹3 crore to ₹41 crore while keeping losses at ₹10.7 crore.

📢Power Talk

“What is most telling is that more than 50% of our CTV watch time in India is on content 21 minutes or longer. This signals that premium, long-form storytelling is thriving on the big screen, fuelled by a unique co-viewing phenomenon where multiple generations enjoy high-quality content together,” Gunjan Soni, Country Managing Director, YouTube India

📚Reads and Recommendations

CollabX drove 320K direct orders for Domino’s India using micro-influencers, proving influencer marketing delivers $5.78 per dollar spent, far from the vanity play 79% of brands still can’t measure. Creators are now paid per conversion, not per post, and performance replaced popularity- influence became infrastructure.

Social commerce resurfacing in India looks like a comeback story, but the real shift is upstream. Discovery has moved from search bars to feeds, creators, and short video, while checkout quietly stays with marketplaces. Platforms like Wishlink win by riding creator distribution instead of rebuilding commerce stacks.

Of course, revenue demands proof, and in India, that means battling 60% fake followers. Growth at 25% annually isn’t creator hype; it’s accountability infrastructure separating influence from theatre. Brands pay for conversions now while fake audiences starve.

DSG Consumer Partners and V3 Ventures circle ₹20 Cr checks for fragrance startups doing ₹2 Cr monthly revenue, chasing a ₹1,500-4,000 price gap while KKR already bought Fogg for $625M in 2021 at ₹1,200 Cr revenue. VCs call it premiumisation as Gen Z leaps from deodorants to EDPs, ignoring that the gap exists because mass buys ₹100 Fogg and premium buys ₹10,000 Chanel.

🔥That’s all for this week! As always, share this with your fellow D2C hustlers, and let’s keep the community growing.

PS: Folks at some companies have told us this newsletter is almost mandatory weekly reading for their teams 🥰. If your company is not in on it yet, get your teams on the latest in the e-commerce space every week.