👶Kid Commerce. Quick Deliveries.

Beastlife's Raise, Vetic's Numbers, DailyObject's Demand

Two juries in two US states just called Meta the new Big Tobacco. Children addicted to feeds, $60 billion in profit, and now a courtroom reckoning. In Delhi, Electronics & IT Minister Ashwini Vaishnaw flagged kids’ social media access as a “major concern,” with regulation talks already underway.

Same week, same Meta quietly shipped a buy-now button inside Instagram ads and rolled out creator affiliate commissions. Every Indian D2C founder’s playbook starts with a Reel and ends with a ROAS dashboard. The platform where they built their entire discovery funnel is now defending itself in the dock. Your storefront is now someone else’s courtroom exhibit.

Courtrooms move slowly. Commerce doesn’t. Here’s the week.

🗞️Marketplace Buzz

Flipkart Minutes is burning through dark stores at 100 a month, and the timing makes the real priority clear: building an IPO story around a $60–70 Bn valuation, not a profitable quick commerce business. An AOV of ₹750–800 is being driven by electronics, a category that does not repeat at grocery frequency. Minutes is burning faster than it earns. Public markets will want unit economics, not just expansion speed.

Swiggy hiking its platform fee to ₹17.58, the exact number Zomato landed on last week, confirms that India’s food delivery duopoly has stopped competing on per-order pricing. A fee that was ₹2 in 2023 is now ₹17.58, and the customer had nowhere to go through each hike. Duopolies always find the price floor together. The ₹1,056 Cr quarterly loss explains more about this fee hike than any press release about unit economics.

Amazon Ads is pitching its full-funnel system as a measurability story, and what it actually reveals is that Amazon now defines ROI for every brand inside it. Awareness spend, purchase signals, and measurement live inside one system; two new AI tools handle the creative and campaigns. That is the business model. D2C brands routing budgets through Amazon’s measurement layer are outsourcing attribution to the entity setting their media cost.

OZi’s $6.2M Series A five months after its seed, is investors betting on one liability: Blinkit and Zepto have never properly curated the kids category (yet). Kids’ shopping is anxiety-driven, repeat-heavy, and category-specific, exactly the three conditions that turn a vertical into a defensible business. Curation alone is the moat. The real question is whether OZi can build enough depth and trust before Blinkit decides the category is worth owning properly.

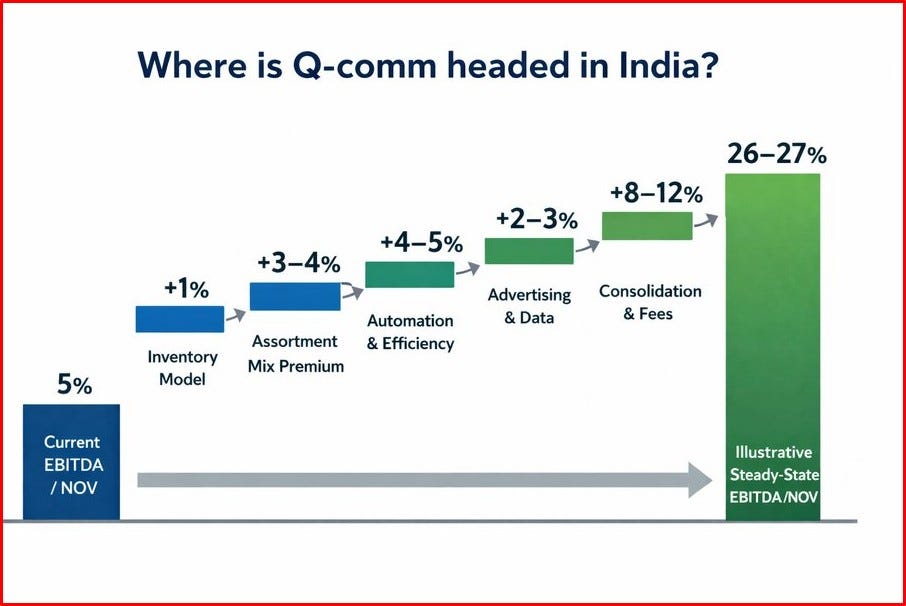

Great take covering the five levers that compound the quick commerce model: inventory ownership, premium mix, dark store automation, FMCG ad revenue, and consolidation pricing power. Add them up, and today’s 5% EBITDA has a probable line to 26–27%. The low-margin read is a snapshot of a business only beginning to unlock its structural model.

Meesho calls Vaani a Gen AI voice assistant, but the product it actually built is the kirana counter online: the assisted shopping conversation that India’s next 500 million users have always needed, and the text-search bar could never deliver. These shoppers don’t browse and filter; they describe, ask, and decide with guidance. A 22% higher conversion rate and 1.5 million users confirm the fit. When the interface matches the behaviour, the category unlocks.

📊Infographica

🍕D2C Snippets

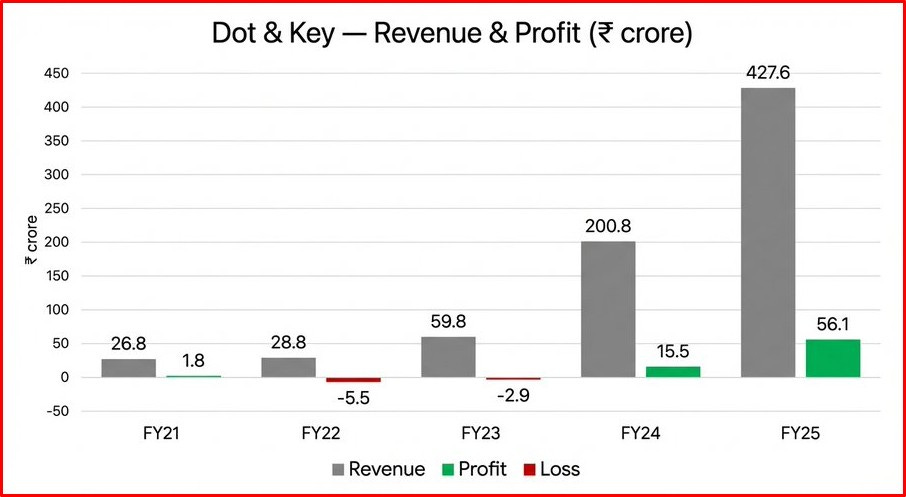

Dot & Key turned ₹1 Cr of founder capital and 200+ investor rejections into ₹1,900 Cr annualized GMV, ₹427.6 Cr revenue, and ₹56.1 Cr profit in FY25. The founding insight, that India had no serums or sunscreens built for Indian skin, was the moat before the money arrived.

Fast&Up owner’s ₹300 Cr Series D going into digestive health, sleep support, and protein-based nutrition tells you where the real category bet is: everyday Indian wellness, not sports nutrition alone. With losses halved to ₹13 Cr on ₹256 Cr revenue, the operating model is ready for the bigger stage. Sports nutrition wins gyms. Every day wellness wins homes. Fast&Up earned the distribution trust; this raise buys the right to walk into a much bigger room.

BeastLife’s ₹20 Cr pre-Series A at ₹320 Cr valuation reads as another influencer-to-brand capital raise, but a 2024-founded brand that is already net profitable and targeting ₹100 Cr in FY26 has the sequence inverted. Gaurav Taneja was the distribution before BeastLife shipped its first product, which means CAC was structurally lower than any nutrition brand could build from scratch. The playbook is different. Profitable before institutional money in nutrition means the founder is the moat.

Vetic’s FY25 financials show revenue growing 2.5X to ₹62.9 Cr as the company expanded to 40+ vet clinics across 10 cities, a trajectory that earned it a Bessemer-led Series C. The other number is ₹65.6 Cr in losses, nearly matching topline, at ₹2.10 spent per ₹1 earned. Pet care is a real category. The capital efficiency question is whether $45 million and 40+ clinics get Vetic to unit economics before the runway ends.

Kidbea’s ₹100 Cr ARR is real, but the ₹30 Cr Series A going into 100 brand outlets and 200 multi-brand stores in 24 months is the harder chapter: offline does not run on sustainability positioning. Digital gave Kidbea room to build a bamboo story, but offline judges on replenishment and price. Bamboo got Kidbea here. The brand that cracked premium kidswear online now has to prove it can run retail without the D2C margin cushion.

Libas hitting ₹1,000 Cr ARR while staying EBITDA positive since inception is being filed as a scale story, but the real play is the store architecture underneath: 10 company-owned outlets last year, 28 this year, 50+ next year, all at ₹3,500–4,000 per sq ft capex. At 1–5% EBITDA margins, every new store is a throughput bet. The category is proven. In ethnic fast fashion, offline is where brands earn the right to hold price.

DailyObjects built 70% own-channel sales before Tier-3 and Tier-4 became a talking point. Now 40-45% of its revenue comes from non-metros — not because it followed a trend, but because it was already there.

📢Power Talk

“At the forefront of channels of the future is quick commerce, the fastest-scaling route to market and a structurally critical channel for the future. It is doubling every quarter and reshaping how consumers discover, shop and replenish.” Priya Nair, CEO & MD, HUL

📚Reads and Recommendations

Meta’s new Buy Now button inside ads compresses the full D2C purchase journey from scroll to checkout into a single tap, and conversion rates will move fast. Every transaction completed before the brand’s site is visited is a customer Meta now understands better, owns longer, and retargets cheaper. The site just became optional. Better conversion today and thinner first-party data tomorrow is the tradeoff every D2C marketer on Meta is carrying right now.

India’s credit card universe just crossed 117.7 million cards, adding 1.05 million in February alone, and it sounds like a D2C founder’s dream. Only February spending data disagrees: YoY growth slowed to 6% from 8%, transaction volumes dropped 8.6%, and banks are rationalising the rewards that drove co-branded checkout. New cardholders are real. Their baskets are just smaller, and the points stack that kept them loyal is getting thinner every quarter.

ChatGPT’s $100M in annualized ad revenue came from less than 20% of eligible US users in six weeks, which means the current inventory is roughly one-fifth of what opens when self-serve access launches in April. D2C brands treating this as a watch-and-wait platform are reading the signal backwards.

Snitch’s CMO has the D2C insight of the year: AI is compressing the discovery funnel into a shortlist of recalled names, not a ranking of optimised bids. Brand recall proxies for trust, and paid visibility can no longer paper over weak fundamentals when AI is the gatekeeper. The algorithm only recommends brands it already knows. D2C brands that treated performance as the whole strategy are about to find AI’s shortlist does not include them.

Luxury fashion label Frances Valentine just dropped a capsule collection with The Colony Hotel in Palm Beach - caftans, tote bags, tees, and it points to something bigger. Hotels are ditching the sad gift shop and becoming proper retail destinations. The Standard has its own merch shop. The Colony already works with Goop and Dolce & Gabbana. For luxury D2C brands, a hotel lobby now offers something an Instagram ad can't - a guest who chose that location, is relaxed, aspirational, and has their wallet out. Distribution by vibe.

PS: Every founder, operator, and investor who reads this starts Monday with an unfair advantage. Just saying.

Join the 3000+ weekly readers, if this was forwarded to you by a team member.