🐶Pet Puja🐶

D2C Fragrances, Sparky and Cutting Agencies

The internet has spent three years telling brands to make it shorter, snappier, faster- because nobody has the patience anymore. Then India booked out a nearly four-hour film, and the memes told the real story: people packing sleeping bags, yoga mats, and three rounds of snacks for the night show, like they were checking into a hotel. Night shows sold out before the first review dropped.

Attention didn’t die- it got selective. The founders building products and content worth four hours of someone’s life are playing a completely different game than the ones optimising for a six-second hook.

🗞️Marketplace Buzz

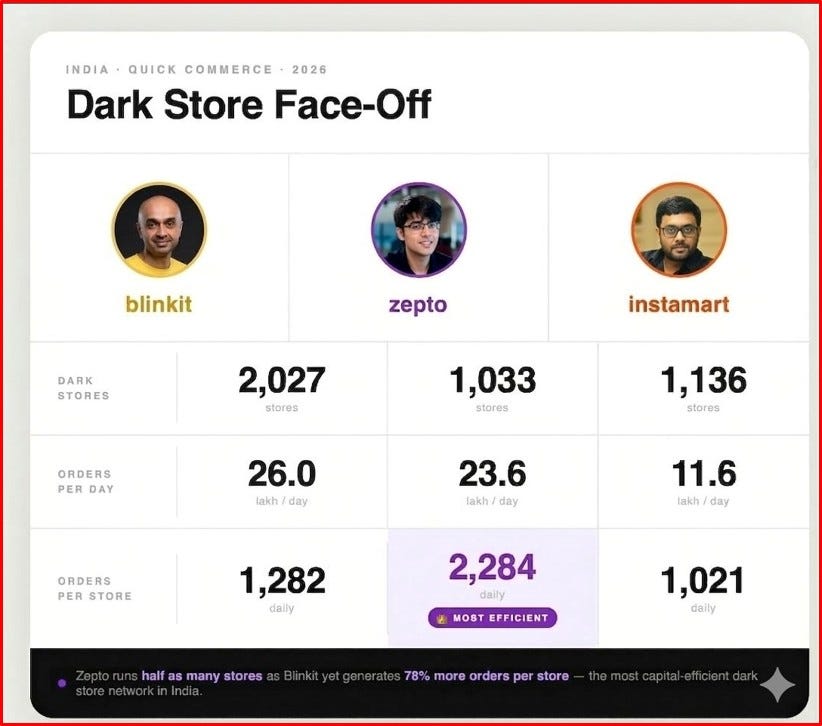

Zepto runs 1,033 dark stores against Blinkit’s 2,027, and the market share chart marks it the clear second player, but 2,284 orders per store per day against Blinkit’s 1,282 tells a completely different story about which business model is defensible. Blinkit built its lead through store count; Zepto built its advantage through yield per store. (The numbers are still being debated by the competition) The gap is 78%. In quick commerce, per-store productivity is the number that predicts who survives the next serious capital correction.

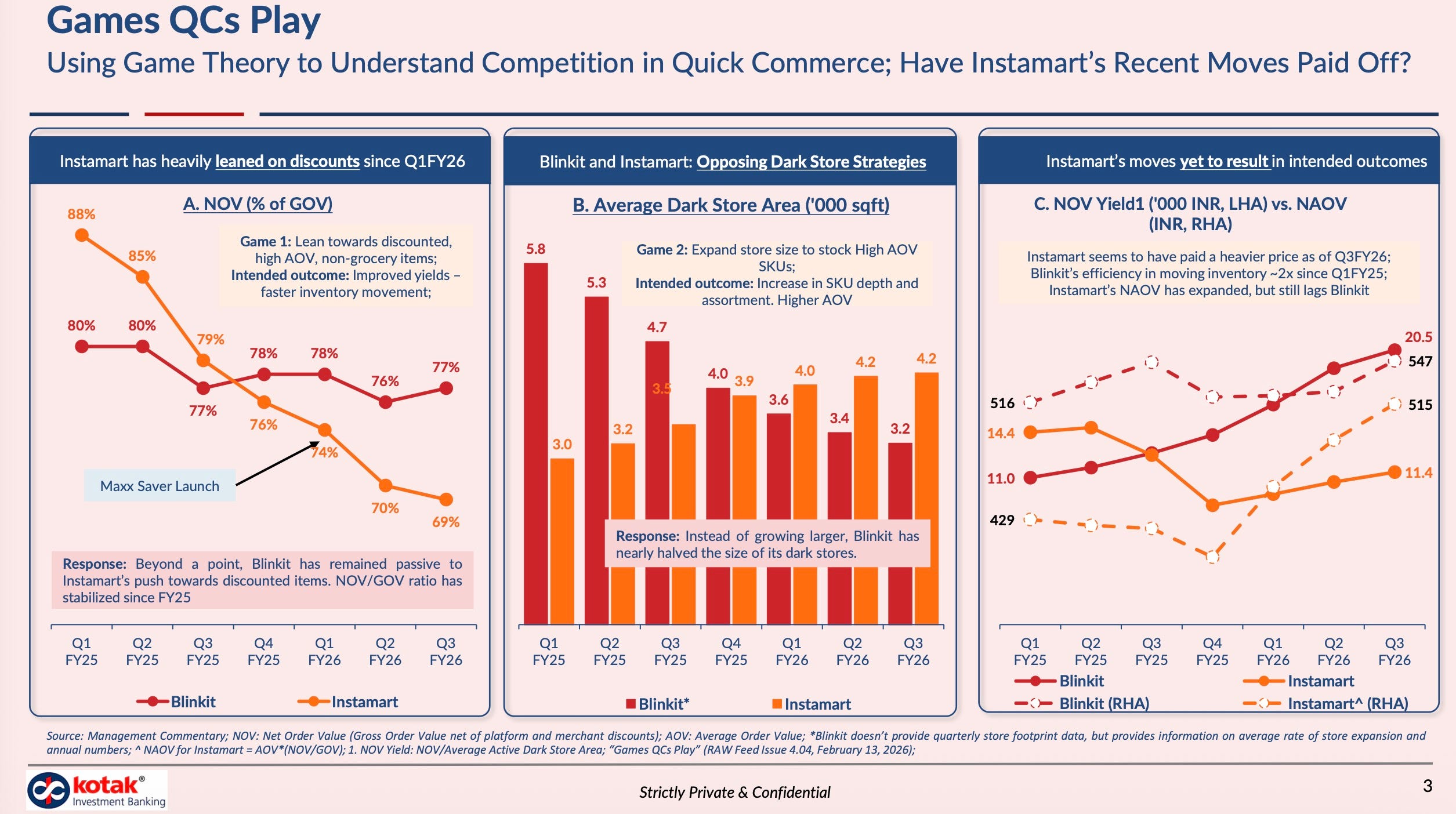

Blinkit watched Instamart run two conscious strategic bets: leaning into discounts since Q1FY26 and expanding dark stores to chase higher-value SKUs, moves Blinkit largely ignored, while shrinking its own stores and keeping margins stable. The result: Instamart’s inventory yield still sits at barely half Blinkit’s, and order value still lags. Blinkit’s move was not to move.

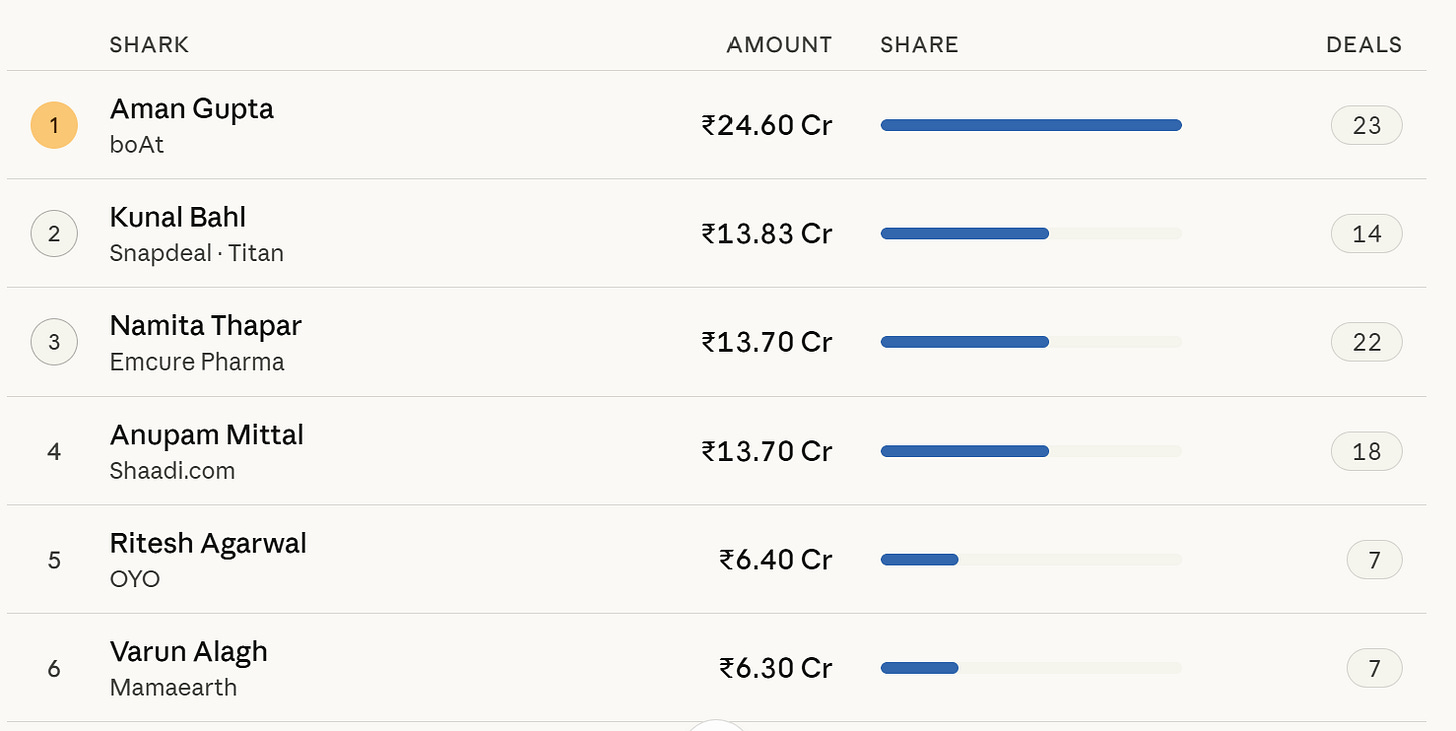

Shark Tank India Season 5 just wrapped with a campus special, and the numbers are in. Of 152 pitches, 73 startups secured deals, with total commitments of Rs 94.88 crore. Aman Gupta led the pack -23 investments, Rs 24.6 crore committed, living up to his reputation as the tank's most trigger-happy shark. Namita Thapar and Anupam Mittal tied at Rs 13.7 crore each, while Kunal Bahl punched in Rs 13.83 crore across 14 deals.

📊Infographica

🍕D2C Snippets

L’Oreal circling Innovist at ₹4,000 crore reads as a D2C exit story, but the contrast underneath it delivers the actual signal: L’Oreal India’s growth fell from 30% to 5% in three years while Innovist posted 182% revenue growth and its first profit in FY25. An eight-year-old digital-first brand now commands a price legacy distribution never could.

Anveshan’s valuation doubling to ₹900-1,000 crore is being positioned as a clean-food investing moment, but quick commerce quietly took revenue from ₹75 crore to a ₹325 crore annualised run rate in a single year. Three prior funding rounds built the brand; one channel built the business. Capital always follows distribution proof, and every clean-label founder watching this raise should be fixing their eyes on the channel, not the cheque.

Zoomies and Moe Puppy both closed pre-seed rounds this week, and the back-to-back timing reads as competitive crowding, but the accumulation beneath it is more specific: a market growing at double FMCG rates, clean-label positioning across both brands, and Moe Puppy already carrying a 30% repeat at 1 lakh customers. India’s petcare category has investor attention, but no scaled brand to anchor it.

Pinq Polka’s ₹4 crore raise in a ₹50,000 crore innerwear market lands as a funding snippet, but nine years of building, 19X growth, and ₹20 crore in revenue inside a category projected to hit ₹90,000 crore by 2031 tells the real story. No D2C brand has come close to cracking scale here. India’s innerwear category is structurally wide open, underpenetrated by D2C, and waiting for its defining brand.

Betterhood’s ₹5 crore seed in preventive musculoskeletal care registers as a niche wellness entry, but back, neck, shoulder, and knee pain collectively burden the majority of working-age Indians, and the category still has no scaled D2C brand to address it. 60,000 customers since October 2024 confirm the demand is real and waiting. Preventive pain care in India is where gut health was three years ago: wide open and underpriced.

Laani’s ₹9.1 crore pre-seed arrives with 500-woman research behind the product brief and Reckitt, Purplle, and Dr. Sheth’s operators in the cap table: category insiders backing a thesis that Indian personal care has spent decades importing formats built for a different consumer. Indian weather, Indian skin, Indian habits: the product brief has always been distinct. Brands solving India-specific personal care from first principles own their category before anyone can copy the brief.

Quick commerce killing offline has been D2C’s most anxious debate for two years, and Pee Safe just closed it with actual operating data: q-comm share jumped from 8% to 30% of revenue in two years while the same pin codes kept growing across offline simultaneously.

DrinkPrime raised ₹20 crore and grew revenue 54% to ₹72 crore in FY25, and the funding narrative will dominate, but the model underneath it is the actual story: IoT-enabled rentals at ₹349 per month with installation and maintenance baked in creates a switching cost that product-sale models structurally cannot replicate. 2 lakh households don’t churn easily. D2C hardware brands that own the service relationship own the customer permanently.

📢Power Talk

“Quick commerce hasn’t cannibalised offline. The same pin codes are growing across both channels, which shows omnichannel brand reinforcement rather than substitution.”- Rithish Kumar, Co-founder, Pee Safe

📚Reads and Recommendations

Noice is accumulating something Haldiram’s and Britannia have never had access to: real-time hyperlocal data on which regional snacks move in which pin codes and at what basket sizes. 300+ SKUs and premium pricing in unbranded categories make this less a private label play and more a category creation engine. D2C brands competing in snacking should be watching this more closely than any legacy FMCG company is.

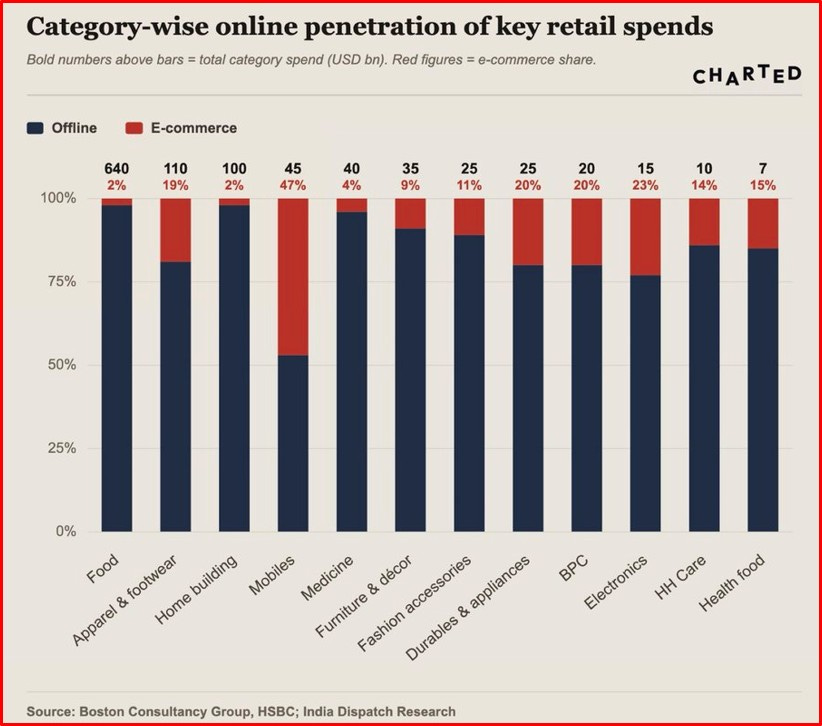

The categories D2C has obsessed over, BPC at 23% online penetration, fashion accessories at 11%, and electronics at 14%, are India’s most competitive and also its smallest by total retail spend. Food commands $640bn with 2% e-commerce share; home building holds $100bn at the same 2%.

D2C brands “cutting agencies” has become the quarter’s favourite disruption story, yet 75% of brands in India never hired an agency at all, and a ₹10,000 crore influencer market has been running largely founder-direct for years. The agency model was always sized for enterprise budgets and brand-level retainers. D2C never fit that shape. Nano creators, DM-sourced deals, half-price closures: that’s the original playbook, just finally large enough to earn a headline.

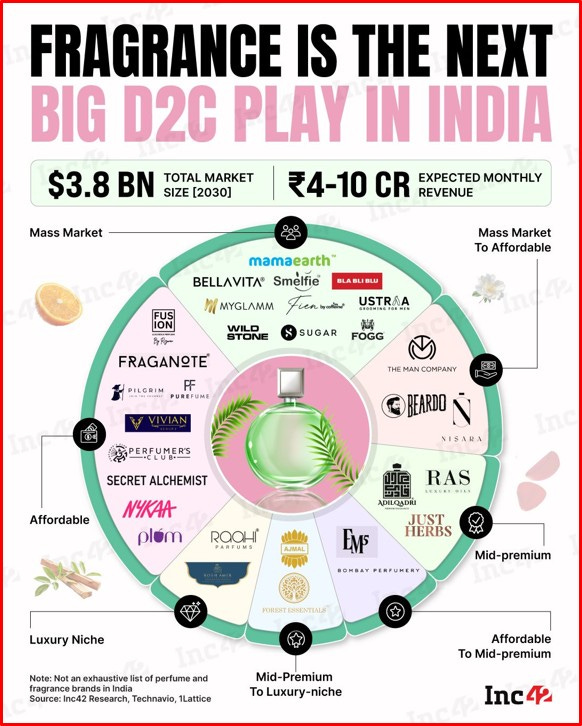

India’s fragrance category is being called an emergence story, but Suryakumar Yadav fronting a perfume brand, Shark Tank cheques landing on another, and Unilever quietly backing a third tells a different story: the race to own mid-premium fragrance in India is already underway, with 25+ brands competing across every price tier in a $3.8 billion market by 2030. Founders still treating fragrance as a whitespace play are entering a category that already has its starting gun fired.

McKinsey’s finding that growth is decelerating across 85% of global CPG categories sounds like a category crisis, but Mamaearth at ₹1,800 crore, Lahori Zeera reshaping beverage, and mCaffeine building a category from scratch reveal the actual structure: incumbents are decelerating while disruptors compound at 25%+ CAGRs. Bold cultural messaging, relentless product innovation, and digital fluency aren’t startup traits anymore - they’re the only traits that are generating category growth anywhere in CPG right now.

When Shein faced a labour conditions backlash, it responded with factory tour content, and made things spectacularly worse. Marketing experts call it a textbook example of what not to do. Cynical audiences coming in hot will scrutinise every frame, every corner, every worker's face.

Walmart and OpenAI's "Instant Checkout", where shoppers could buy directly inside ChatGPT, hit a wall. Onboarding merchants was messy, errors were frequent, and barely 30 Shopify merchants made it live. Now both sides are quietly pivoting. OpenAI is scrapping native checkout and instead building dedicated retail apps inside ChatGPT that redirect users to the retailer's own site to complete the purchase. Walmart is embedding its own AI assistant Sparky into ChatGPT and Gemini. The dream of the AI agent that just buys stuff for you? Still a dream. Check out, it turns out, is harder than conversation

PS: Folks at some companies have told us this newsletter is almost mandatory weekly reading for their teams 🥰. If your company is not in on it yet, get your teams on the latest in the e-commerce space every week.