🚀 The Stack Keeps the Money 💰

Musk's Trillion & Zepto's DRHP, Flipkart's Vanishing Moat

Elon Musk just became the first human worth a trillion dollars.

SpaceX went public this week at a $1.77 trillion valuation, the largest IPO in history that pushed one man past twelve zeros. His fortune now runs roughly four times the next-richest person alive.

Musk captured a trillion because he owns the whole stack: the rockets, the factory, the launch pad. India’s D2C founders have built something just as hard, real brands and real demand conjured from scratch, while the model quietly routes most of the upside to the layer underneath: the ad platforms, the marketplaces, the logistics rails.

That 2-5% margin ceiling is a map of ownership. The stack just keeps the money. The value you build is real, and most of it pools one layer down.

However, even the most powerful LLM model on earth learned this week that whoever owns the rung above you can switch you off with a single message, no warning, no appeal (for now).

So build the brand, and also own the rails beneath it. That is the whole game. Let’s get into it. 👇

🗞️Marketplace Buzz

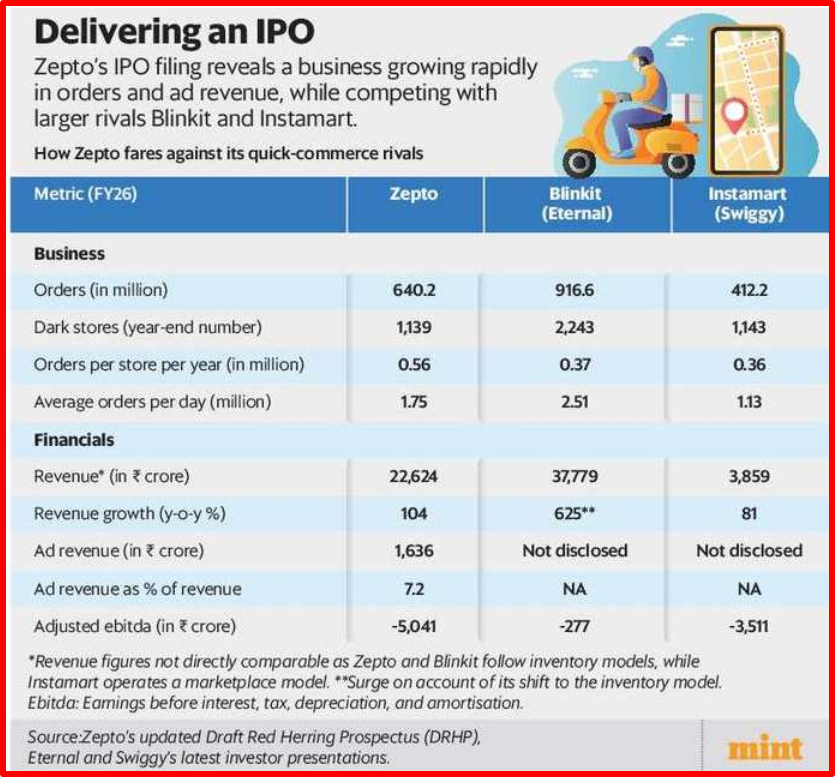

Zepto filed to go public as a grocery story, but stack the DRHP lines and a different company falls out: ₹1,636 Cr in ad revenue, up 2.5x in a year, fed by 2,468 brand partners, and the only line that prints margin. The dark stores lose money so the ad desk does not have to. Groceries are the audience, brands are the customer. Zepto is a retail-media business doing grocery as customer acquisition.

And while doing so, Zepto is also asking investors to score it on density and cash flow per order instead of the basket-size yardstick its rivals made standard. The numbers it steers away from are exactly the ones that sting: a ₹330 basket against Blinkit’s ₹525, a ₹1,248 Cr loss against Blinkit’s ₹37 Cr profit. Clearly, new scorecards flatter their author.

BazaarNow just pulled in a ₹72 Cr round to scale what everyone is calling quick commerce, but strip away the label and it is really a tier II grocery-habit engine in disguise. No coupons, no wallets, no discount circus, just vernacular search and call-to-order shopping built for households metros forgot. While the big players burn cash chasing ten-minute glory, BazaarNow is quietly teaching small-town India to reorder without a single coupon.

📊Infographica

🍕D2C Snippets

Uni Seoul just raised ₹35 Cr, and the easy read is another founder surfing the K-pop wave into Indian carts. But follow the money, and a steadier story shows up: offline stores, supply chain, private label, the unglamorous plumbing of a physical retailer. The trend bought the attention, and now the store economics have to keep it. Korean design is the hook on the window, but the business being built is old-fashioned shelf discipline at scale.

Supertails is expanding vet clinics and a pharmacy because retail margins do not pay, and healthcare returns twice as much. Pet food was the acquisition layer; the clinic is where money is made. The model already shows it: healthcare is a fifth of the Bengaluru business at double the margin, while revenue of ₹308.3 Cr still carries a widening ₹52.5 Cr loss. While selling products bought the customer, only healthcare turns that customer into a profit.

Manam Chocolate just raised $9M to open more premium stores in Delhi-NCR, but the real bet sits far upstream, in the cacao farms and fermentation sheds it actually owns. While global cacao buckles under climate shocks, owning origin in West Godavari turns a supply headache into a moat. The pretty bars are the storefront, but really, the farm is the franchise. Most chocolate brands rent their beans; Manam grows the whole tree itself.

Emami is back to its oldest move, writing a ₹500 Cr cheque for D2C brands to jump-start a top line that has quietly gone flat. The logic is tidy: when the core slows, buy growth that is easier to find than to build. The brands are not the hard part- however, what decides whether any of this works sits deeper in how the house is run, and that is the question a cheque does not answer.

📢Power Talk

“The market for customized or personalized beauty and personal care products is very niche in India at the moment, and even globally, it is not a big segment,”- Swapneela Biswas, principal at Kearney.

📚Reads and Recommendations

Indian D2C reads as a brand-building decade, but stack the numbers, and a harsher truth emerges: 2-5% net margins for the best operators, CAC climbing 15-20% a year, and a 99% mortality rate before any real exit. Brands cap near 2-12x revenue while the picks-and-shovels layer clears 8-20x. The plumbing keeps the money.

Amazon and Flipkart spent a decade teaching India to open their app first, and agentic AI is now turning that discovery moat into the one thing a chatbot can lift out of their hands. The ads and the ₹15 to ₹25 they skim off every ₹100 order live at the front door, which is vanishing. The boring fulfilment stack is suddenly the only moat a middleman cannot reorder around.

DTC is the one game where everyone read the trend correctly, and yet most still go home broke. The theme was always the easy part, the ticket that got you noticed; the brands that compounded quietly built an engine behind it: retention, distribution, the boring machinery nobody posts about. The theme gets you in the room.

🔥That’s all for this week! As always, share this with your fellow D2C hustlers, and let’s keep the community growing.

PS: More than 4,000 founders, operators, and investors who read this start their Monday with an unfair advantage. Just saying.